Devon-BPX Breakup

Quick Thoughts on the Eagle Ford split

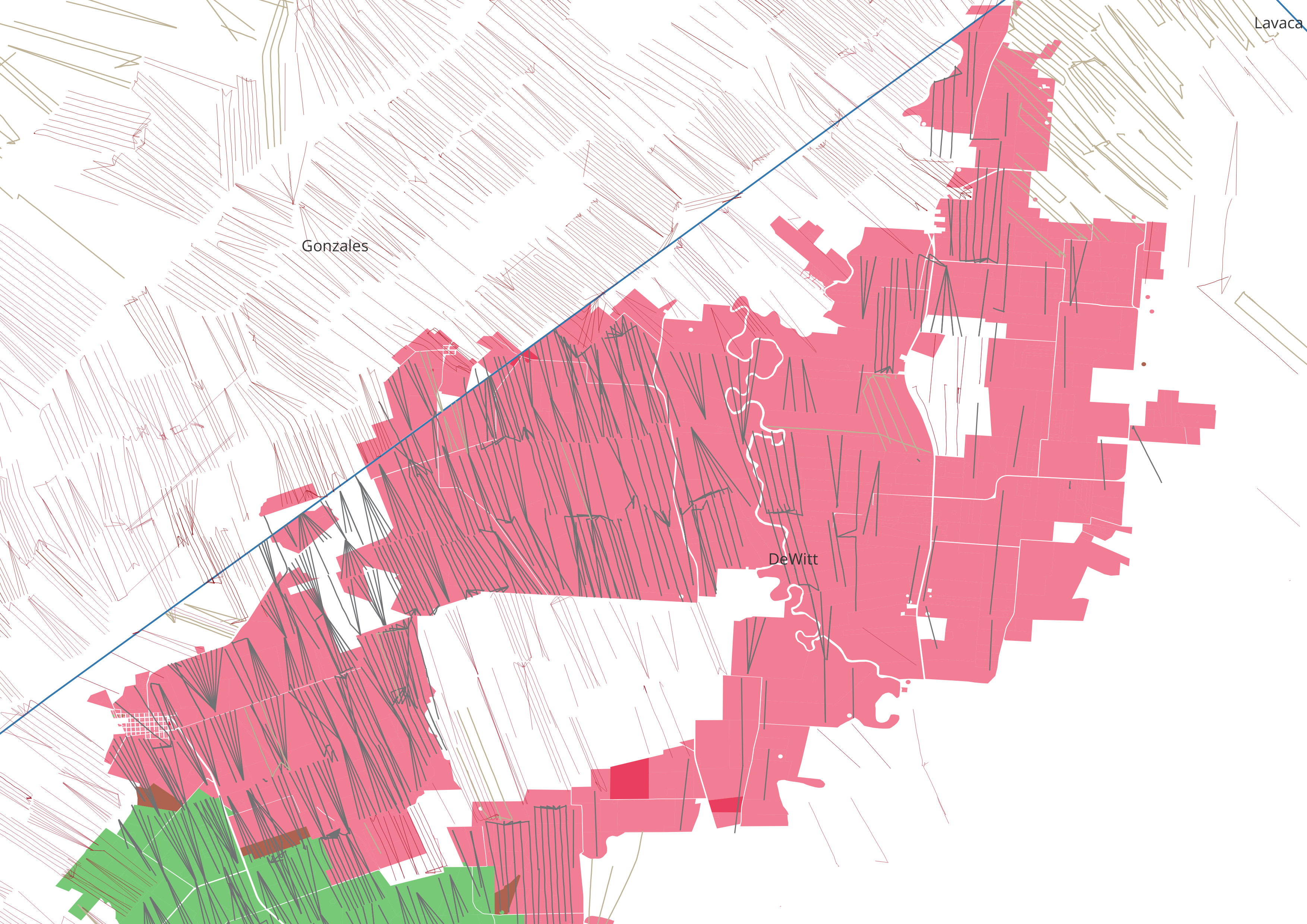

Perhaps because I was deep into building mode in January, I missed the initial news on the ending of the BPX/Devon JV in the Eagle Ford, which was mostly focused on DeWitt county. As of April, the previous 50% split has now been separated into largely two distinct blocks, with Devon grabbing the NE portion and BPX retaining SW.

JV Background

The JV was originally structured in the early days of the Eagle Ford (2010) between Petrohawk and Geosouthern. The Petrohawk portion passed from BHP and then to BP, while Geosouthern was acquired by Devon in 2013.

For some insane reason that probably made sense at the time, BPX (Petrohawk) had control of development, while Devon (Geosouthern) was responsible for the well after it went to sales. Nothing says “efficient JV” like two cooks who don’t share a kitchen.

Dissolution

Fast forward to this year, Devon, perhaps realizing the lack of new decent M&A opportunities out there and still digesting Grayson Mill, decided it was time to gain operatorship for a portion of the acreage. My money is largely the latter, as the company really does need to begin realizing more value from their scattered, existing asset base, and the Eagle Ford is pretty heavily-developed on their position.

Sell-side estimates pegged the cash consideration paid to BPX to be in the ~$250 million range. If you look at the acreage map, most of the remaining development exists on the DVN block, so it was some combination of PDP-value split and remaining development upside.

Company comments

This was a bit fun to read, but both clearly thought they won this trade.

A key value driver for us to dissolve this JV was that we are confident that we can save more than $2 million in D&C costs per well with improved well design, supply chain and application of operational technology from our other basins. The combination of this cost reduction and control of the go-forward development significantly enhances returns and provides a material uplift to the NPV of our position. - Clay Gaspar, Devon incoming CEO, Q4 2024 Earnings Commentary

and in the Q&A

Yeah. It's interesting. I mean, I think this is a classic win-win opportunity. When I summarize it and we displayed a map, when you think about the assets that BPX is going to inherit and then the assets that we inherit, objectively, they valued more of those assets than we do, and we have valued more of the assets that we're going to inherit. And so there was a natural accretion associated – mutual accretion associated with this deal. I think above and beyond that, I think about our ability to control pace, to really direct the operations. And then, as I pointed out in the prepared remarks, we see material operational improvement, and we've already displayed that. We've got – since we've taken over the rig, we have one well down, we have another well exactly on pace where we thought it should be. And that yields more than $2 million per well and value creation straight from the top on all of the remaining opportunities ahead, which obviously is a massive needle-mover.

I would have to say first on the list as we run the waterfall and think about the value creation for us, there's no doubt about it. Saving $2 million-plus per well off the top is roughly about $2 million of NPV per every single well out there. So that's a real opportunity for us and certainly is the headline approach for us. But controlling the pace is really valuable as we think about how quick these wells – we drill these wells in seven days. And so, being able to control that when we need to, being able to back off when we have the opportunity to. I know refracs aren't the hottest topic du jour, but I can tell you there is real material value. And as we see more and more value creation from this – this is what we call as magic rock, it continues to yield more and more opportunities. And that's what we're really excited about. But again, I'll reiterate, I think this is a mutual win-win. Sometimes you bring together these joint ventures and you see the opportunities there. By the same token, opportunities can change, evaluations can change, technology can change, motivations can change. And it can be time to disillusion. I mean, a similar analogy is, selling midstream assets and buying midstream assets back in, both can be right at the given time. I would say when I think about the BPX opportunity, this is the right move for them now, and this is the right move for us now.- Clay Gaspar, Devon incoming CEO- Clay Gaspar, Devon incoming CEO

Clearly, Clay things this acreage is “magic rock” and that they can drill it for $2 million less than BPX. We’ll touch on that a bit later.

Yeah, so it was a great deal. We're really, really excited to get it done and I mentioned it in the presentation—Enverus quoted about quarter billion dollars of value kind of coming our way as a result of the deal.

I think that comes in a couple of parts. The main part is we started with 10 [MMbbl/d] more production than they're starting with. So that's driving a lot of value today. The other part of that is there's a lot of overhead charges …, et cetera, that we are going to get some efficiencies from that doesn't show up in those, kind of, external numbers. We're also getting some advantages from marketing from our trading and shipping team, dollars per barrel, if you will, from a sales price. That's really a huge advantage to us. And I think when we look at the asset and how it's split, we think we ended up with a better subsurface than some of our partners did. And really the Devon, the Northeastern part is a little bit more challenging. We view that as needing three strings, which requires a little bit more cost, three drilling strings to really get the reliability and execution that we desire and really be able to drive the long laterals that I was talking about in the assets. So we think we've got a little bit less complicated area, a little bit better subsurface and a team that's really going to get after it and extract the value. - Shawn Holzhauser, VP of Development at BPX

So, largely Holzhauser (correctly) points out that their acreage position is better quality from a productivity perspective, and points to the difficulty drilling on the Devon portion and requirements of 3-strings. Though Clay does not mention this, it is likely where the bulk of the cost savings assumptions come from (ie trying to drill this portion of acreage on two strings). Additionally, reading between the tea leaves, BPX seems to imply that Devon is overcharging on managing production and that they could do a much better job of marketing the product (also likely quite true).

Devon acreage

Devon’s revised portion is 46,000 net acres at ~95% WI. The company reports ~700 undrilled locations in the Eagle Ford, but did highlight 550 of those in Blackhawk. Where are those locations? Well, zooming in, you see that most of those development locations are to the Southeast. If you know anything about the Eagle Ford, you’ll realize that that lack of development is due to both a) poorer productivity and a b) deeper horizon (usually requiring three strings of casing and higher cost) that is much gassier.

The wells that aren’t to the southeast and that are closer to the core will be much more heavily down-spaced, and I for one don’t want to drill wells 8-16 in an existing Eagle Ford section.

I mentioned poorer productivity.

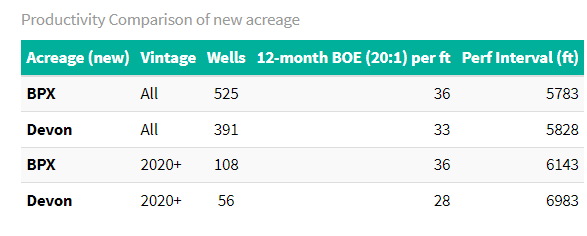

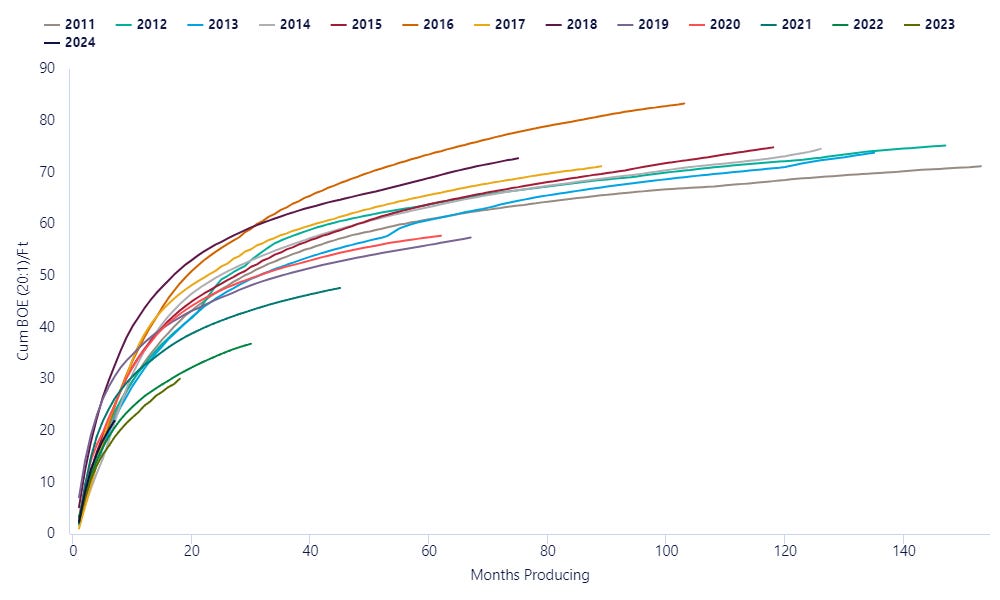

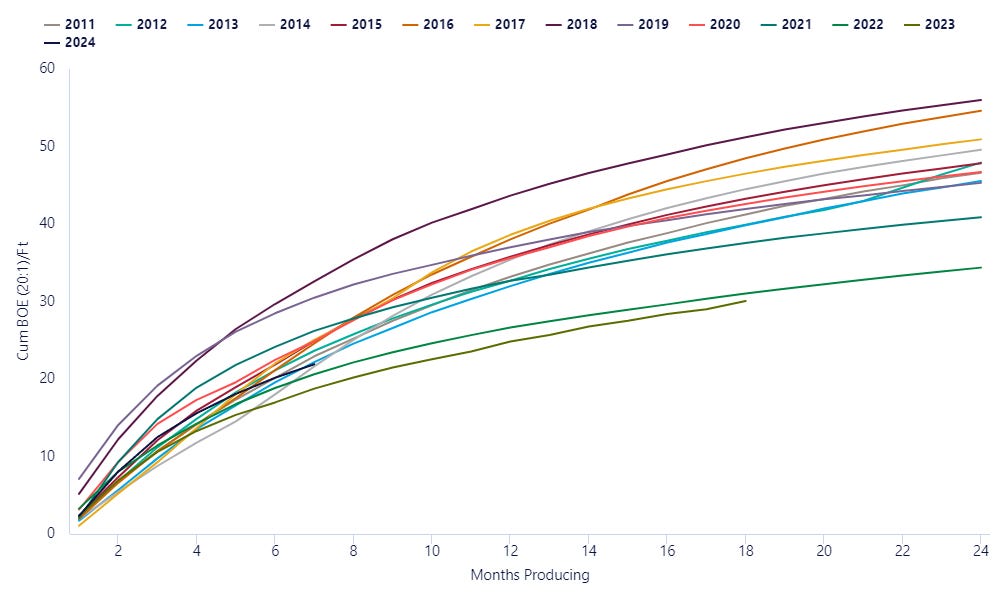

Productivity on the BPX portion is historically ~10% better, though since 2020 the Devon acreage has declined in productivity significantly. Regardless, it’s clearly not as strong.

Legacy acreage on the new Devon side has had its’ worst four years in 2021-2024 (as seen in the cumulative boe/ft plot below); once again why I don’t want to drill downspaced locations, and why the actual way Devon realizes value from this acreage is trying to prove up the SE portion of the position.

I won’t spend much time on the BPX acreage. They largely received cash and a PDP stream. What remaining locations they have are probably better quality, but they are mostly downspaced and there are much fewer.

On to the capex savings

To be honest, in most plays I look at with our capex data, BPX is by-far the highest cost operator, perhaps validating that reputation as a gold-plater. And I fully expected that to be the case here.

But, the data tells a different story.

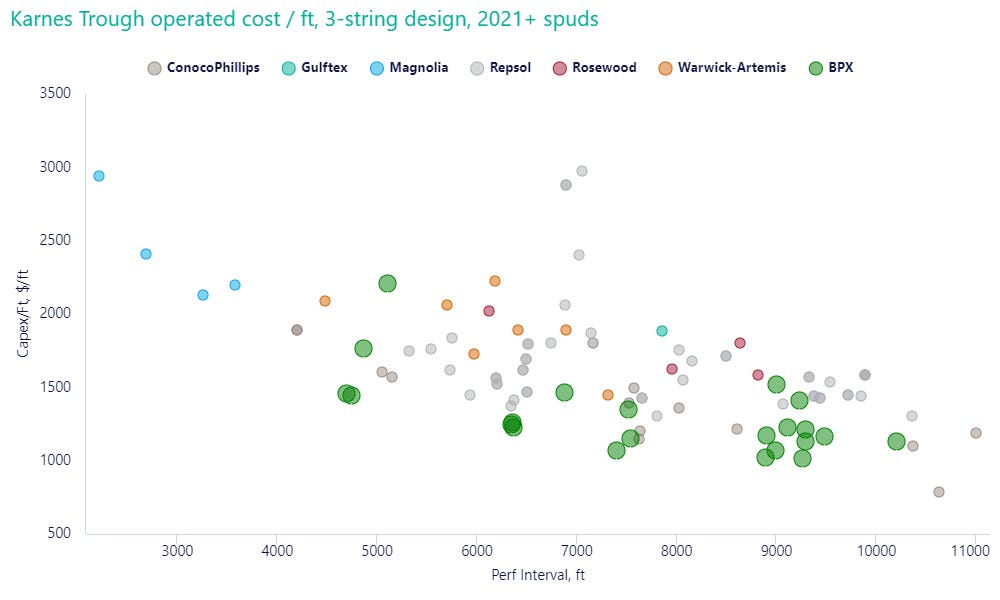

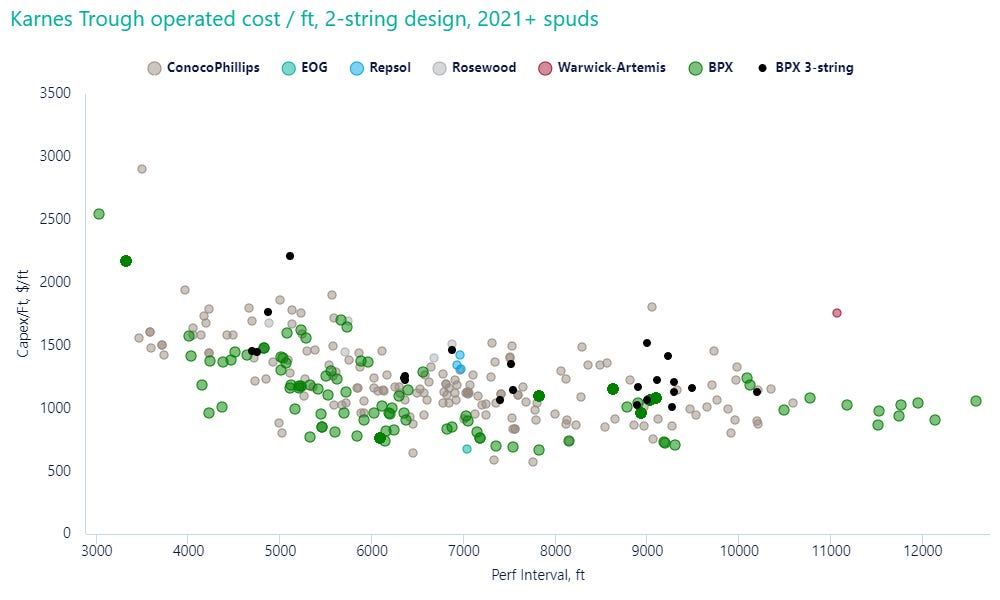

From a cost/ft perspective (2021+), BPX is generally better than the other operators, though they do spend a bit higher on 2 mile/2-string locations.

So, given BPX is bucking their own reputation and drilling, at worst, on-trend wells, how is Devon going to save upwards of $2 million/well?

For the most part, BPX focused on 2-string designs on the Devon acreage at depths less than ~12,600 tvd, while going with 3-string when you head deeper. Now, why would they willingly spend more money to add another string?

When BPX drilled in the deeper Karnes Trough they often shifted from a 2-string to a 3-string design to manage narrower pore pressure windows and wellbore stability. The extra intermediate casing allows them to isolate overpressured or fractured zones, minimize losses, and maintain safe kick tolerance. It’s basically a risk management tool: the upfront cost is higher, but it can save a lot of trouble compared to stuck pipe or sidetracks in deeper, hotter parts of the play.

My guess, Devon is calculating that cost savings as wells where they think they can go the 2-string route and manage those risks, and perhaps they’re right. But, where it will get very risky is that much deeper portion of the acreage where the bulk of remaining inventory sits. That sits at 13,500 ft TVD and deeper, so that will get a lot hairier.

So what is the real rationale?

Devon’s motivation is probably more about portfolio control and operating leverage, though the headline “capex savings” are trying to help justify it to the market more. They can align drilling to maximize their own supply chain savings, apply consistent well designs, and manage the pace to fit their balance sheet goals. It also makes it easier to optimize the tail-end development or even divest the position later, since there’s no JV to untangle. Just watch for cost overruns on that deep acreage.

What is AFE Leaks? We are an independent research and data platform that focuses on transparency for Lower 48 oil and gas wells — from detailed AFE capex breakdowns to product revenues to financials. We combine verified cost data with unbiased analysis to help operators, investors, and analysts benchmark spending, spot hidden risks, and squeeze more value from their unconventional portfolios.

Also, for giggles, I had AI research and write a report on the JV. How’d it do? Maybe all of these have been written by AI. Maybe I don’t actually exist.

Report on the Dissolution of BPX Devon JV in Eagle Ford Shale (2025)

Table of Contents

Introduction

Background of the Joint Venture

Formation and History

Key Players

Details of the Dissolution

Announcement and Finalization

Post-Dissolution Structure

Economic Implications

Cost Savings

Operational Efficiencies

Production Guidance and Financial Adjustments

Strategic Focus and Future Plans

Devon Energy's Shift Towards Organic Growth

BPX Energy’s Enhanced Oil Recovery Initiatives

Conclusion

Follow-Up Questions

1. Introduction

In February 2025, Devon Energy and BPX Energy announced the dissolution of their long-standing joint venture in the Eagle Ford Shale's Blackhawk Field, a partnership that had been in place for 15 years. This report delves into the implications of this dissolution, focusing on both economic impacts and strategic shifts for the involved companies.

2. Background of the Joint Venture

2.1 Formation and History

The joint venture between BPX Energy and Devon Energy regarding the Eagle Ford Shale was initially established by Petrohawk Energy and GeoSouthern Energy. Over the years, this partnership was inherited by the two companies and focused on joint exploration and production efforts in the Blackhawk field.

2.2 Key Players

This JV brought together significant resources and expertise from Devon Energy and BPX Energy, thereby enhancing their operational footprint in one of North America's most productive oil regions. Throughout its duration, the joint venture navigated various market cycles, adapting to industry shifts both operationally and strategically.

3. Details of the Dissolution

3.1 Announcement and Finalization

On April 1, 2025, the dissolution of the joint venture was finalized, allowing Devon Energy to assume operatorship of about 46,000 net acres in the field, with a working interest greater than 95%. This decision was highlighted as a pivotal moment for Devon, signaling a strategic shift in focus toward independent operational control.

3.2 Post-Dissolution Structure

Post-dissolution, Devon Energy’s full control is expected to have immediate and long-term ramifications for its operational strategy and financial performance. The immediate transition is accompanied by Devon taking over existing drilling operations, allowing for streamlined processes and decision-making.

4. Economic Implications

4.1 Cost Savings

One of the most significant immediate advantages cited by Devon Energy is the expected savings of over $2 million per well in drilling and completion costs. Early data from operations under Devon’s control showed a remarkable 40% increase in drilling speeds paired with nearly a 50% reduction in costs on initial operated pads.

4.2 Operational Efficiencies

The dissolution is anticipated to bring about enhanced operational control for Devon, providing it with the flexibility to allocate capital more effectively. With the previous constraints associated with joint operations removed, Devon is poised to implement optimized drilling, investment, and completion schedules that reflect their own strategic priorities.

4.3 Production Guidance and Financial Adjustments

As a direct outcome of the dissolution, Devon raised its 2025 production guidance by 1%, projecting to average 815,000 barrels of oil equivalent per day. Additionally, their capital expenditure budget was reduced by $100 million to $3.9 billion, reflecting improved efficiency gains from the separation of operations.

5. Strategic Focus and Future Plans

5.1 Devon Energy's Shift Towards Organic Growth

Under the leadership of incoming CEO Clay Gaspar, Devon Energy is embracing a more organic growth strategy, pivoting away from acquisitions and focusing on maximizing internal efficiencies and operational enhancements. This new direction seeks to realize the value embedded within Devon's existing asset portfolio instead of pursuing outside growth opportunities.

5.2 BPX Energy’s Enhanced Oil Recovery Initiatives

Conversely, BPX Energy is shifting focus toward enhanced oil recovery (EOR) projects within the Eagle Ford region. They plan to utilize advanced recompletions and refracturing techniques in an attempt to achieve up to a 25% resource recovery increase, having identified over 400 candidates suitable for these initiatives. This move indicates a recognition of the need to innovate and focus on recovery optimization in a changing market environment.

6. Conclusion

The dissolution of the joint venture between Devon Energy and BPX Energy represents a significant turning point for both companies, especially within the context of the Eagle Ford Shale. Amid evolving market conditions, the transition appears aimed at optimizing operational efficacy and capital allocation while strategically repositioning for future growth.

In summary, Devon’s acquisition of complete operational control allows for enhanced flexibility, while BPX's focus on EOR initiatives indicates an adaptive strategy to maintain competitiveness. Both companies stand to benefit from their new operational landscapes as they navigate through challenges posed by both market dynamics and technological advancements.