AFE Leaks Pulse

May 18, 2026

Mostly international/Alaska news this AM, as I really can’t find much of note. I suppose read it as post-earnings breather. I have heard separately that M&A is heating up in the backend, so we’ll probably get some good announcements before too long.

On the AFE Leaks front, we are revising some of the MCP-related offerings and expanding just what it can do (working on getting permits into the fold there, as it’s in the database and now queryable in our V2 API endpoints),

I’m putting out a video soon as I walkthrough what you can do via the MCP. People don’t like to admit it, but we’re all using chat models now, and having a Q&A layer to our database that you can access while working in the terminal/their harness is I believe the direction of travel for much of this new way of working.

We’re also firming up our inventory model so that we can actually have go-forward estimates and honestly a PDP forecast for either:

Our company profiles

Private assets that are either on the market or ones we can postulate that will be.

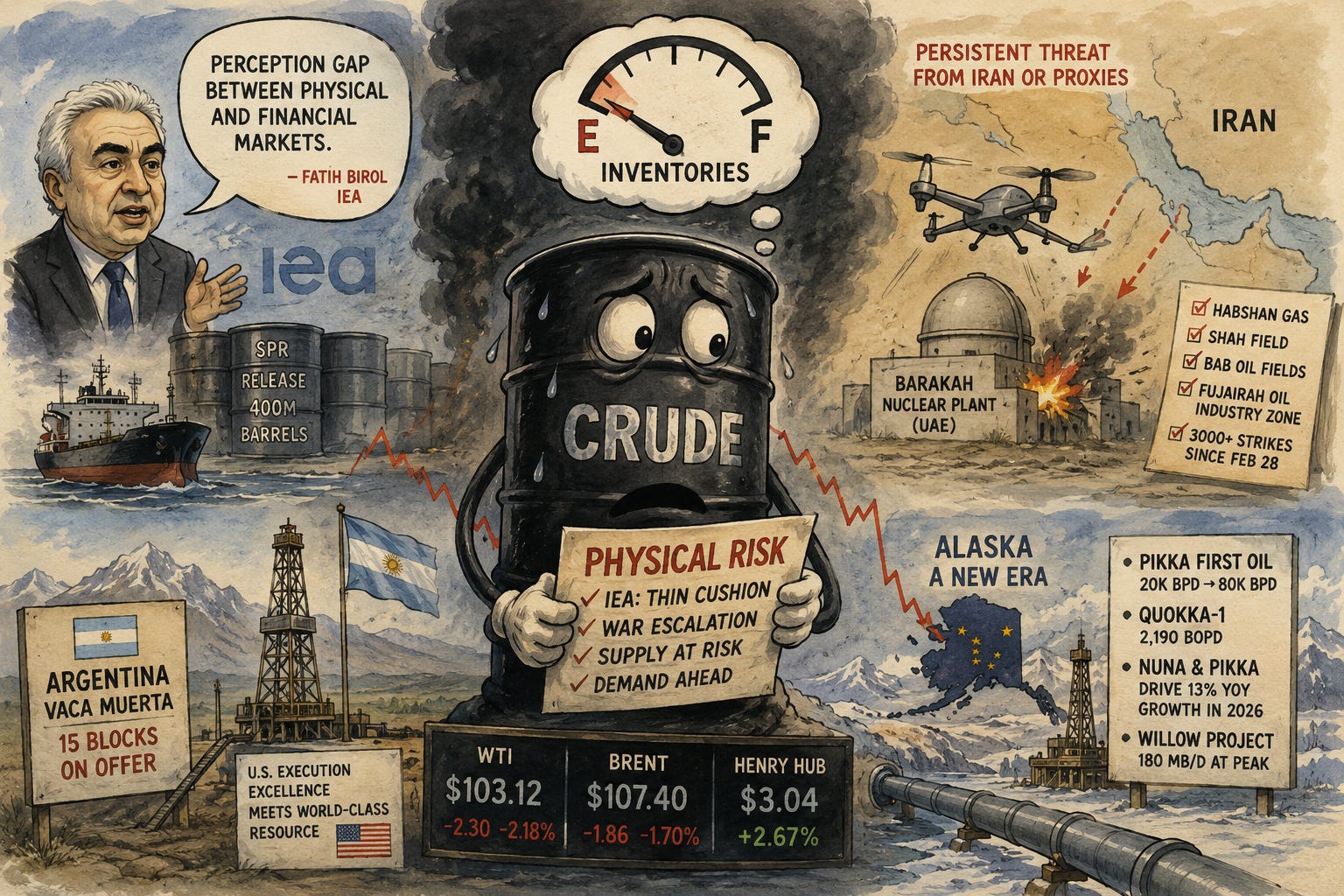

Crude is selling off this morning into an information environment that, by my read, argues the other way. WTI is $103.12 (-$2.30, -2.18%) and Brent $107.40 (-$1.86, -1.70%) as of 8:48 AM EDT. Henry Hub is up 2.67% to $3.04/MMBtu. Geopolitical movements all push the same direction on physical risk, and the tape isn’t reflecting them.

Birol says the cushion is thin

On the sidelines of the G7 finance meeting in Paris this morning, IEA Executive Director Fatih Birol told reporters commercial oil inventories are “depleting very fast” with several weeks of cover remaining. His framing in the meeting itself was a “perception gap” between the physical and financial markets — the same point he made last month when he warned Europe could run out of jet fuel in roughly six weeks.

The IEA coordinated a 400-million-barrel SPR release in March, the largest in its history; ~164 million barrels had been delivered by May 8, equivalent to about 2.5 mmbpd into the market. Birol’s point is that these reserves aren’t endless and the demand call into northern hemisphere planting and summer travel hasn’t yet hit. The agency also cut its 2026 supply forecast — global supply now seen falling 3.9 mmbpd across 2026 due to the war, against a prior estimate of 1.5 mmbpd.

Barakah crosses a line

Three drones entered UAE airspace from the western border Sunday morning. Two were intercepted; the third hit an electrical generator outside the inner perimeter of the Barakah Nuclear Energy Plant in the Al Dhafra region. No radiological impact, no injuries, and emergency diesel generators powered Unit 3 while operations continued. The UAE has not publicly attributed the strike and noted the western-border origin, which complicates the default Iran assumption.

Two things to flag. First, this is the first strike on a peaceful civilian nuclear facility in the Gulf, and the IAEA has been explicit about it — Grossi called for maximum restraint near any nuclear plant. Second, since the war began February 28, the UAE reports more than 3,000 ballistic, cruise, and drone strikes from Iran or aligned proxies, with prior hits already taken at Habshan gas, the Shah field, Bab oil fields, and the Fujairah Oil Industry Zone. Sheikh Abdullah bin Zayed condemned Sunday’s attack and signaled the UAE retains full right to respond. Trump is reportedly meeting top national security advisers Tuesday on Iran options.

Vaca Muerta looking to Rise

Argentina has launched its largest Vaca Muerta acreage round since 2016, offering 15 exploration blocks across the play through Neuquén provincial company GyP — more than double the six blocks offered in the previous provincial auction. In places, the Vaca Muerta can compete with the Permian on well productivity.

CLR’s recent 90% acquisition of the Los Toldos II Oeste block and farm-in to Pan American Energy assets is the most visible US shale entry into Vaca Muerta to date — a Bakken pioneer importing its play-development model into a basin with comparable productivity and a fraction of the surface and capital intensity. With US-based execution excellence in the fold, you could begin to see the country push breakevens in the VM lower.

Alaska: Pikka first oil and a state-level inflection

Santos and Repsol announced first oil from Pikka Phase 1 on the North Slope this morning. The development targets the Nanushuk and will ramp to 20,000 bpd over the next few weeks, then hold roughly a month until the Seawater Treatment Plant comes online for water injection. Plateau of 80,000 bpd is expected in Q3. Twenty-eight development wells drilled at first oil, 21 stimulated and flowed back in line with pre-drill expectations. Santos operates with 51%, Repsol holds 49%.

The companion data point is Quokka-1, six miles east of Pikka in the Quokka Unit. A 4,787-ft TD well into the Nanushuk, ~143 ft net oil pay at 19% average porosity, single-stage frac flowing 2,190 bopd. Santos is now planning a two-drill-site Quokka development with capacity comparable to Pikka Phase 1, and was carrying 177 MMboe of 2C contingent resource for Quokka at year-end 2025.

Pikka at plateau is roughly 19% of current Alaska output. The EIA’s November STEO has Alaska crude reaching 477 Mb/d in 2026 — a 13% YoY increase, the largest annual increase since the 1980s — driven by Nuna (peaking at 20 Mb/d, currently around 7 Mb/d) and Pikka. ConocoPhillips’s Willow is a separate, larger story still — $8.5-9 billion committed, 180 Mb/d at peak, first oil 2029. The leading indicator was the March 18 NPR-A lease sale, which drew a record $163.7 million in high bids across 11 companies on 187 tracts covering 1.33 million acres, with ExxonMobil’s surprise re-entry and a Repsol/Shell partnership winning 42 tracts. Alaska has been in structural decline since 1988; recent movements suggest it won’t be for long.