AFE Leaks Pulse

Diamondback first to break rank, DVN/CTRA approved, Meta wants some of that sweet Permian gas

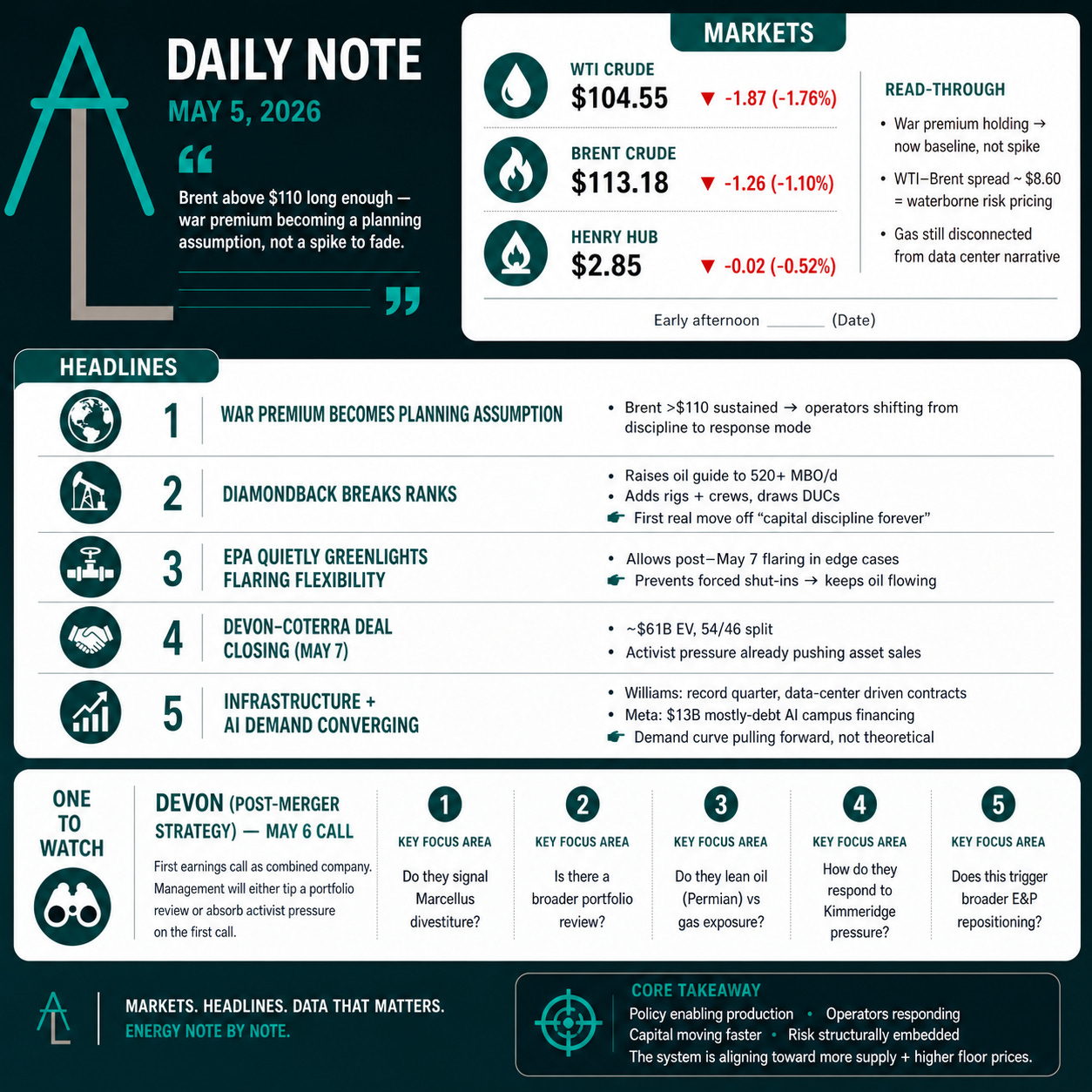

Brent has held above $110 long enough — Iran still gripping the strait, Project Freedom now live under fire — operators are beginning to treat the the war premium as a planning assumption rather than a spike to fade. EPA's quiet clarification last week that producers can keep flaring associated gas past the May 7 phase-out deadline reads less as regulatory housekeeping than as a green light: the administration wants the taps open and is removing the friction one rule at a time. Yesterday, Diamondback became the first major independent to actually move — lifting full-year oil guidance to 520+ MBO/d, adding two to three rigs, running five completion crews, and explicitly drawing down DUCs to hold the line. The rest of earnings season tells us whether anyone follows.

Markets

WTI was trading at $104.55, down $1.87 (-1.76%). Brent was at $113.18, down $1.26 (-1.10%). Henry Hub was at $2.85, down $0.02 (-0.52%).

Crude is off modestly this morning despite the Hormuz escalation — read it as the market giving Project Freedom a small benefit of the doubt on Day 2, with the WTI–Brent spread still wide at ~$8.60 reflecting the geopolitical risk concentrated on waterborne barrels. Henry Hub at $2.85 remains the underwhelming read against the data center demand narrative; the gas thesis is contracted-growth and long-dated.

Diamondback Q1 + Production Raise

FANG averaged 521 MBO/d in Q1, beat its own guide, and used the print to raise full-year 2026 oil guidance to 520+ MBO/d (from 500–510) and total BOE to 972+ (from 926–962). Capex moves up to ~$3.9B from ~$3.75B. The guide raise is a discrete shift from the "discipline forever" framing and the first clear sign that one of the most capital-disciplined Permian operators is leaning into the tape. Capital returns held the line — base dividend up 10% to $4.40/yr, $548M of buybacks, $777M of long-dated notes repurchased at ~81% of par.

The watch is whether this is idiosyncratic or directional. WTI has been north of $100 for weeks now on the Hormuz premium, and to date the Permian peer set has held the line on capital discipline despite the price signal. Diamondback breaking ranks first matters precisely because they were one of the loudest discipline voices. The independent peer group largely reports over the next two weeks and we’ll see who is joining the party.

EPA Flaring Guidance

EPA issued guidance May 1 clarifying that current regulations already allow routine flaring of associated gas at new oil wells in limited circumstances after the May 7, 2026 phase-out deadline. The agency framed it as responding to operator concerns out of the Williston and Permian — circumstances "outside their control" forcing shut-ins. DOE's number for what gets preserved: tens of thousands of bbl/d. This sits on top of the April 4 final rule that revised two technical aspects of the 2024 rule (industry savings ~$208M/yr through 2038), with more amendments in the queue.

Lease-level economics where Waha gas trades negative are a math problem: paying to move molecules is worse than burning them, and any regulatory headroom on flaring widens the window where operators don't shut in oil to comply with gas-handling rules. It does not solve takeaway constraints, but it removes a constraint that would have forced curtailments this summer if Permian gas got squeezed again before Blackcomb fills. Read it as the regulatory companion to Diamondback's guide raise — the administration is making clear it wants the taps open.

Devon / Coterra Shareholders Approve, Deal Closes May 7

Both shareholder bases waved the merger through with overwhelming margins (>98% Devon, >99% Coterra per the StockTitan approval announcement), and the deal got approved May 4, with close on Thursday. Final terms unchanged: 0.70 Devon shares per Coterra share, ~54%/46% pro forma ownership, ~$61B combined enterprise value (debt included), Houston HQ. The combined company will be one of the largest Delaware Basin operators with material additional positions in the Anadarko and Marcellus.

The interesting development is what Kimmeridge did the week before close. Their April 28 open letter to the future board called for accelerated non-core divestitures and a more "decisive, shareholder-focused" strategy from day one — a continuation of their long-running push for Coterra to exit gas-weighted Marcellus and Anadarko positions. Devon's Q1 call on May 6 will be the first earnings call as the combined entity, which puts management in the position of either tipping a portfolio review or absorbing the activist pressure on the first call.

Scout Energy → Jonah, $1B+ Western Anadarko

Scout Energy Partners closed the divestiture of its Western Anadarko Basin position for over $1B (but let’s not confuse it with the Cherokee play). The release named the buyer as undisclosed; Hart Energy reporting confirms it as Jonah Energy. The package is sizable and integrated: ~250 MMcfe/d (gas, NGL, and helium) across roughly 3 million acres, paired with three gas processing plants, 7,200+ miles of gathering, and ~400,000 HP of compression.

Williams Q1 — Record Quarter, Data Center Tailwind

Williams put up a record quarter and the contract book confirms why. GAAP net income $864M (+25% YoY), adjusted EBITDA $2.254B (+13%), AFFO $1.770B (+22%), and management guided to the upper half of the 2026 EBITDA range. The drivers are higher Transco net rates and expansion volumes, new Gulf production tying in, and gathering volume growth out West.

The contracted growth tied directly to power demand is what stands out. Per the Williams Q1 release: Power Express was upsized to 750 MMcf/d, Atlas added a 164 MMcf/d Northeast data center contract, Silver Spur on Northwest Pipeline added 275 MMcf/d, and ~700 MMcf/d of Marcellus and Haynesville gathering expansions are in motion. The same release disclosed Project Neo — a $2.3B, 682 MW behind-the-meter power project — and the commissioning of the Aristotle pipeline supporting Plato South.

Meta — $13B El Paso Financing, Mostly Debt

Meta is working with Morgan Stanley and JPMorgan on roughly $13B in financing for the El Paso AI campus, targeted at 1 GW with a 2028 in-service date, per Bloomberg's reporting. The package is a large majority debt with a smaller equity slice — potentially one of the largest single-site digital infrastructure financings ever assembled.

The structure is the story. Meta's willingness to lever a single-site, single-operator project at this size signals that hyperscalers are now optimizing for speed of capacity over balance sheet purity. If MSFT, GOOG, and AMZN follow with comparable debt-heavy structures, the long-dated power demand curve gets pulled forward — capital availability stops being a gating factor and shifts the bottleneck back to power, gas, and grid.

Hormuz — Project Freedom Goes Live

The US launched Operation Project Freedom on Monday to escort stranded commercial vessels out of the Gulf via Omani waters, after Iran's months-long closure of the strait left roughly 2,000 vessels and ~20,000 seafarers stranded per IMO estimates. CENTCOM has guided-missile destroyers and active mine-clearance operations behind the effort. The first day was contested: per Reuters, Iranian forces fired missiles, drones, and small boats at US destroyers (USS Truxtun and USS Mason both transited under sustained fire and were unhit), and a UAE oil storage facility at Fujairah took drone damage. Brent moved sharply on the escalation.

The floor under crude is structural as long as ~20% of seaborne oil and ~20% of LNG remain at risk of intermittent disruption — Brent at $113 and the wide ~$8.60 WTI–Brent spread are the tape pricing that risk in real time. Mines, fast-attack boats, and shore-based AShM batteries don't need to close the strait to keep insurance rates and tanker premiums elevated, which itself reroutes flows and supports prices. The longer this goes on, the more that floor moves up.

One To Watch — Does Anyone Pay Up For Devon's Marcellus?

Kimmeridge has now publicly put a Marcellus divestiture on the agenda before the merger has even closed. The combined Devon will inherit a Marcellus position that is among the most heavily developed in NEPA/SWPA — high-quality rock, but mature, PDP-weighted, with the value embedded in producing wells rather than undeveloped inventory.

The question for next week: when Devon issues its first set of post-merger guidance and commentary, does management hint at a portfolio review, or do they hold the line?

Sources

Diamondback Q1 + Production Raise

Diamondback Energy press release (May 4, 2026): https://www.diamondbackenergy.com/news-releases/news-release-details/diamondback-energy-inc-announces-first-quarter-2026-financial

Reuters: https://www.reuters.com/business/energy/shale-producer-diamondback-energy-beats-first-quarter-profit-estimates-2026-05-04/

EPA Flaring Guidance

EPA press release (May 1, 2026): https://www.epa.gov/newsreleases/epa-clarifies-when-oil-and-natural-gas-producers-can-flare-after-phase-out-deadline

Offshore Technology: https://www.offshore-technology.com/news/epa-eases-rules-oil-gas-sector-phase-out/

World Oil: https://worldoil.com/news/2026/5/1/epa-allows-limited-routine-flaring-at-new-oil-wells-under-updated-rule/

Devon / Coterra Merger + Kimmeridge

Devon/Coterra shareholder approval announcement: https://www.stocktitan.net/news/DVN/devon-energy-and-coterra-energy-shareholders-approve-wsodba45lzue.html

Kimmeridge open letter (April 28, 2026): https://www.prnewswire.com/news-releases/time-for-action-kimmeridge-releases-letter-to-the-future-board-of-devon-energy-302755651.html

S&P Global Market Intelligence: https://www.spglobal.com/market-intelligence/en/news-insights/articles/2026/4/investment-firm-urges-devon-energy-to-sell-assets-after-coterra-merger-101136080

Scout Energy → Jonah Energy

Scout press release: https://www.businesswire.com/news/home/20260501964771/en/Scout-Energy-Partners-Divests-Over-%241-Billion-in-Assets-in-the-Western-Anadarko-Basin

Hart Energy (Jonah confirmation): https://www.hartenergy.com/energy-market-transactions/acquisitions-and-divestitures/he-scout-jonah-western-anadarko/

Williams Q1

Williams press release: https://www.businesswire.com/news/home/20260504880577/en/Williams-Announces-Record-First-Quarter-2026-Results

Reuters: https://www.reuters.com/legal/litigation/williams-beats-quarterly-profit-estimates-higher-natural-gas-demand-2026-05-04/

Meta El Paso Financing

Reuters: https://www.reuters.com/legal/transactional/meta-taps-morgan-stanley-jpmorgan-el-paso-data-center-deal-bloomberg-news-2026-05-04/

Bloomberg: https://www.bloomberg.com/news/articles/2026-05-04/meta-taps-morgan-stanley-jpmorgan-for-el-paso-data-center-deal

Hormuz / Project Freedom

The Guardian: https://www.theguardian.com/world/2026/may/04/shipping-bosses-nervous-trump-plan-to-guide-vessels-strait-of-hormuz-iran

Reuters (US Navy engagement): https://www.reuters.com/world/middle-east/us-destroys-six-iranian-small-boats-shoots-down-missiles-drones-us-admiral-says-2026-05-04/

CNN: https://www.cnn.com/2026/05/04/middleeast/project-freedom-hormuz-guide-ships-intl-hnk-ml

Al Jazeera: https://www.aljazeera.com/news/2026/5/4/trumps-project-freedom-can-us-navy-guide-stuck-ships-out-of-hormuz

Review-Journal: https://www.reviewjournal.com/news/politics-and-government/us-claims-progress-in-reopening-the-strait-of-hormuz-saying-2-merchant-ships-have-transited-3796636/

International Maritime Organization (IMO), Hormuz vessel backlog statement, May 2026

Tape Data

Bloomberg Markets, captured ~7:25 AM EDT

Disclaimer

AFE Leaks Research and Consulting publishes analysis for informational purposes only. Nothing in this brief constitutes investment advice, an offer to buy or sell securities, or a recommendation to pursue any specific transaction. Figures are sourced from public filings, primary reports, and AFE Leaks proprietary data; verify independently before acting. Views are our own and do not represent any operator, sponsor, or counterparty mentioned.