AFE Leaks Daily Pulse

Hormuz still closed. CLR and OVV print Q1 underneath a $100 strip. KODA hits the market the same week Kraken closes Zavanna. The non-core Bakken just became the most interesting page in the data room.

Commodities

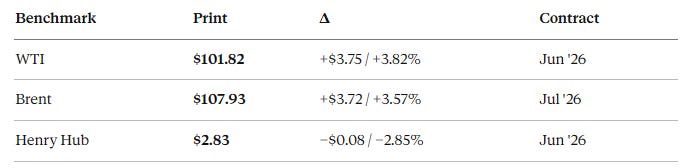

Crude is back above $100 after Trump rejected Iran’s latest counter-proposal as “garbage” and called the ceasefire “on massive life support.” Saudi Aramco’s Amin Nasser told Q1 callers that the market will need until 2027 to normalize if Hormuz stays blocked beyond mid-June, and the IEA described the extended shutdown as the largest supply shock on record. Gas pulls back as the equation shifts — global LNG flows are unsettled, but the prompt month is still digesting a heavy storage build and a soft April weather setup. The crude-gas ratio is north of 36:1.

Earnings: CLR

Continental dropped its 10-Q this morning — and the headline number ($441M net loss attributable to Continental, vs +$316M Y/Y) is entirely a hedge book artifact. The unrealized derivative loss alone was $994M (which we called out a couple of months ago); cash on derivatives was −$114M. Strip the mark-to-market out and the underlying business is fine: oil/gas/NGL revenue of $1.85B, only 2% lower Y/Y despite the Permian rev rolling back 13% to $368M. Powder River was the bright spot at $158.6M, up 20% Y/Y — Hamm’s continued buildout there is starting to print.

Going forward, CLR has 122 Mbbl/d of WTI fixed swaps on for Apr–Dec 2026 at $64.28, plus 33 Mbbl/d of collars with a $69.38 cap. Against a $100+ spot tape, that’s a giant unhedged-only-by-virtue-of-being-private upside transfer to counterparties. The mark-to-market balance sheet shows $869M in net derivative liabilities, vs $381M of net assets at YE25 — a billion-dollar swing in 90 days. Cash is still strong at $1.6B. They did not pay a common dividend in Q1 (vs $628K Y/Y, a tell that they’re prioritizing the balance sheet through the spike).

Capex was the other read: $934M E&D, up 21% Y/Y. Continental is still leaning in.

(CLR 10-Q)

Earnings: OVV

Ovintiv delivered $1.1B in CFO and $634M FCF on $605M of Q1 capex . (OVV Q1 release)

GAAP was ugly: $630M net loss driven by a $1.2B after-tax ceiling test impairment that was almost entirely a function of a weaker SEC 12-month trailing oil price relative to YE25.

The portfolio engineering is the story:

Closed NuVista ($2.8B, ~100 Mboe/d, 930 net 10K’ locations, 140K acres) — heavy Montney weighting.

Closed Anadarko divestiture at $2.85B in early April.

Redeemed the $700M 5.65% 2028 notes April 20 — saves $40M/yr in interest.

Net debt under $3.3B as of April 30, down 40% Y/Y. Net Debt/EBITDA below 0.8x.

Resumed buybacks: $84M in March, $180M YTD through April 30.

Reiterated FY26 guidance: 620–645 Mboe/d production, $2.25–2.35B capex.

Production hit the top of guidance across all four products. Q1 oil & condensate realized $70.14/bbl (98% of WTI). The hedge book is light vs. CLR: ~55–61 Mbbl/d of WTI on for the rest of 2026, weighted to 3-way options with a ~$70 call strike. They’re going to capture meaningful tape upside relative to a more aggressively hedged private peer.

McCracken’s framing on the call this morning: “We’ve built a track record of leading execution efficiency and disciplined capital allocation and now we’ve combined those strengths with best-in-class inventory depth in the two best E&P assets, and a clean balance sheet.” Translation: the portfolio reshape is done; the next 12 months are about converting the dual-engine into buybacks.

Kraken Closes Zavanna; Issues $400M of 7.125% ‘31s

Last night Kraken Resources priced and closed $400M of 7.125% senior unsecured notes due 2031 at par. Proceeds repay revolver, which had funded the Zavanna acquisition (closed March 31). (Kraken release)

Deal mechanics worth flagging:

Acquired entity: Zavanna Energy Operating, LLC, recapitalized in Sept 2024 by Carnelian (replacing the legacy GSO/Blackstone preferred from 2013).

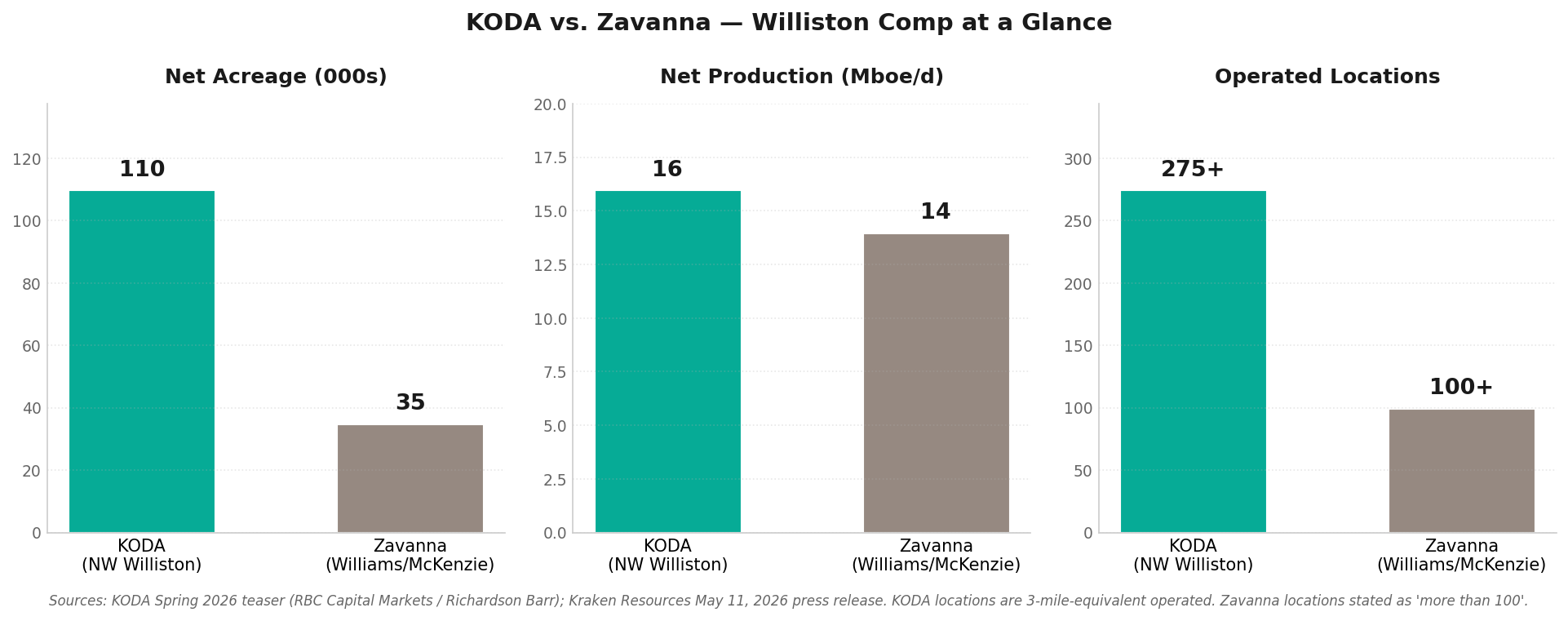

35,000 net leasehold acres, 175 operated wells, more than 100 drilling locations in core areas of Williams and McKenzie counties, North Dakota.

Net production of approximately 14 Mboe per day at closing, plus gathering systems and 11 saltwater disposal wells.

$200 million equity contribution from affiliates of Kayne Anderson and certain members of the Company’s management team.

Total purchase price not disclosed.

Pro forma, Kraken is now the sixth largest producer in the Williston Basin with approximately 18 rig-years of remaining inventory with an average lateral length of nearly 16,000 feet across 404,000 net acres in North Dakota and Montana. The 7.125% coupon on a debut ‘31 print is a clean read on private-Williston cost of capital in a $100 tape — call it ~125–150 bps tighter than where this kind of paper was clearing pre-Iran.

One To Watch — Zavanna comps and what they mean for KODA

We frame Zavanna at an implied $650–800MM EV based on the funding structure — ~$200MM equity plus revolver funding, followed by $400MM of notes — or roughly $46–57K per flowing barrel on ~14 Mboe/d. That gives the cleanest current Williston comp.

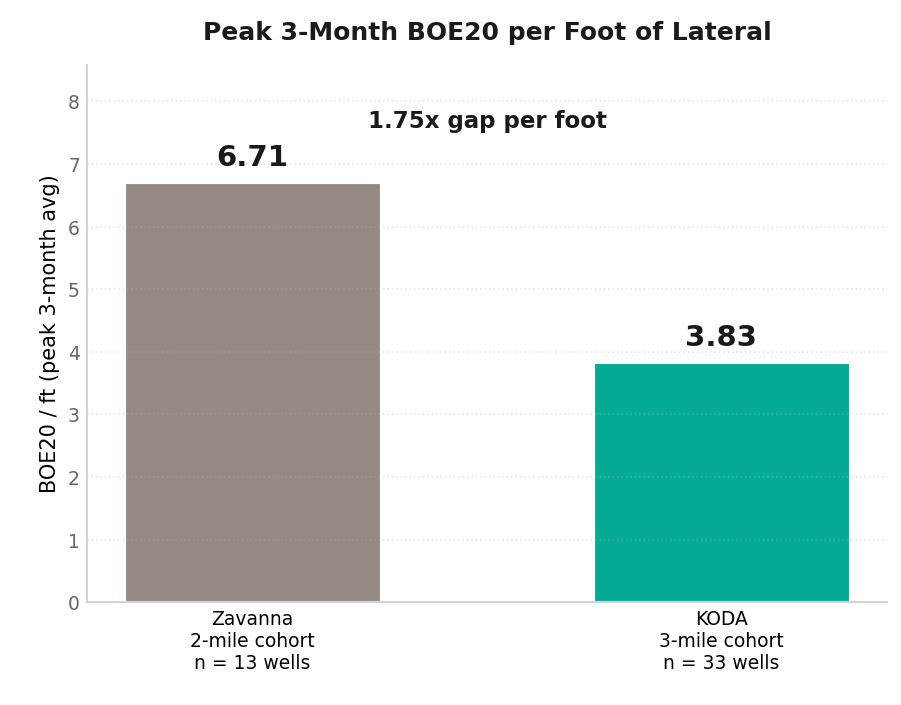

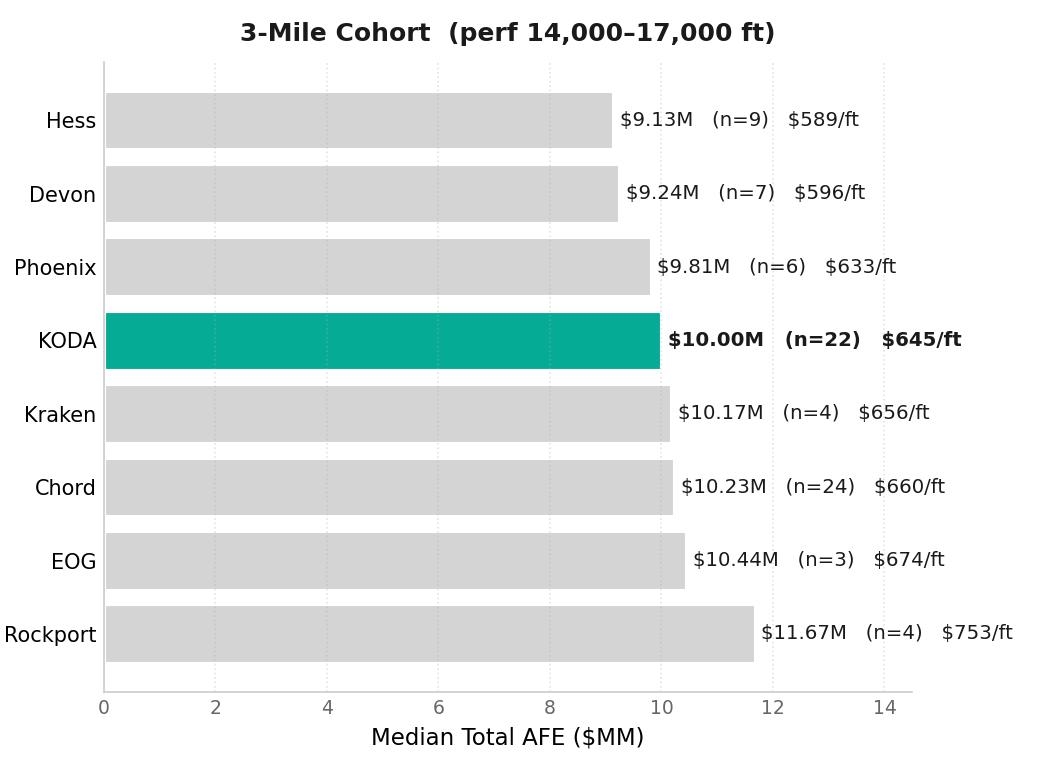

The important caveat is that this is not a simple “Zavanna costs more / KODA costs less” story. Modern Williston AFEs appear to cluster tightly, and Zavanna today likely carries a cost structure much closer to KODA than an older 2-mile comparison would imply. The economic question is therefore not whether KODA can offset weaker rock with meaningfully cheaper wells. It is whether similar capital dollars in NW Williston can generate enough durable recovery to narrow the productivity gap over time.

How the market likely frames it:

Zavanna anchor: ~$46–57K per flowing

KODA range: likely discounted from core Williston given maturity / proof risk

Floor: $459MM PDP PV-10

Key discount drivers: less mature long-lateral history, non-core positioning, and long-term strip sensitivity

Our View: This prices on PDP + discounted inventory, not headline location count. 10-20% discount on Zavanna assumed anchor, so 500-700 range. Operators will really have to believe the inventory story. At least there’s not much downspacing risk! Most likely buyer in our view is Chord, given they are apparently aiming to be the last one standing in the basin.

Watch:

VDR opened April 27; first-round bids likely late June

Clearing price will show how much buyers pay for NW Williston long-lateral inventory when cost structure is competitive but curve proof is still developing.

Sources: KODA Spring 2026 Opportunity Overview teaser (RBC Capital Markets / Richardson Barr, Wells Fargo, Houlihan Lokey); Continental Resources Q1 2026 10-Q; Ovintiv Q1 2026 earnings release (Form 8-K Ex. 99.1); Kraken Resources May 11, 2026 press release; AFE Leaks proprietary AFE database (Williams + McKenzie + Divide ND horizontal well AFEs, 2023+ vintage); CNBC, Trading Economics, NLPC, ConocoPhillips IR.